Oil Prices, Shipping and Chip Shortages Could Tighten Philippine Car Supply Through 2026

Rising oil prices, tighter shipping routes, and semiconductor pressure are driving up vehicle costs and delays for Philippine car buyers in 2026.

Why Philippine Car Prices May Rise Again in 2026

Rising oil prices, fragile shipping networks, and intensifying competition for semiconductor capacity are creating a structural supply squeeze for Philippine car buyers in 2026.

As Middle East tensions stretch into their ninth week, the risk is no longer limited to fuel prices; Higher freight costs, persistent chip lead times, and the rapid expansion of AI infrastructure are now converging into a broader automotive supply challenge that could extend well into 2027.

What makes the current environment more serious is that the automotive industry was already dealing with structural pressure before the latest geopolitical shock, as shipping networks remain fragile, automotive chip lead times are still elevated, and AI demand is absorbing a growing share of global semiconductor capacity. For Philippine buyers, that combination could mean higher prices arrive before outright shortages do.

Oil Prices Are Only the First Layer of Risk

Tensions involving Iran and the Strait of Hormuz have already pushed energy markets higher, with Brent crude briefly moving above $100 per barrel, which are felt immediately in import-dependent economies like the Philippines, that immediately raises fuel and logistics costs.

The larger risk is what comes next with higher oil prices increasing the cost of shipping, plastics, chemicals, batteries, and industrial production across the automotive supply chain. Modern vehicles rely on globally distributed manufacturing networks, even moderate disruptions can ripple across pricing, production schedules, and delivery times.

For Philippine buyers, where most vehicles and parts arrive from regional hubs such as Thailand, Japan, China, and South Korea, prolonged disruption could gradually tighten supply across both mass-market and high-tech vehicle segments.

The pressure on automakers now extends far beyond fuel costs, with semi-conductor bottlenecks, shipping volatility, battery materials, industrial metals, and specialty gases are all becoming interconnected risks within the global automotive supply chain.

Automakers are being squeezed from both sides: oil shocks are lifting costs, while AI demand is absorbing chip capacity.

While a wide range of materials from rare earths to battery metals could affect vehicle production, not all risks are equally immediate. In the current environment, three pressure points stand out: shipping, semiconductor supply, and the growing competition from AI for chip capacity. These factors are already under strain, closely linked to rising energy costs and geopolitical disruption, and are likely to have the most immediate impact on vehicle availability, pricing, and delivery times in the Philippine market.

Shipping Delays Could Be the First Warning Sign

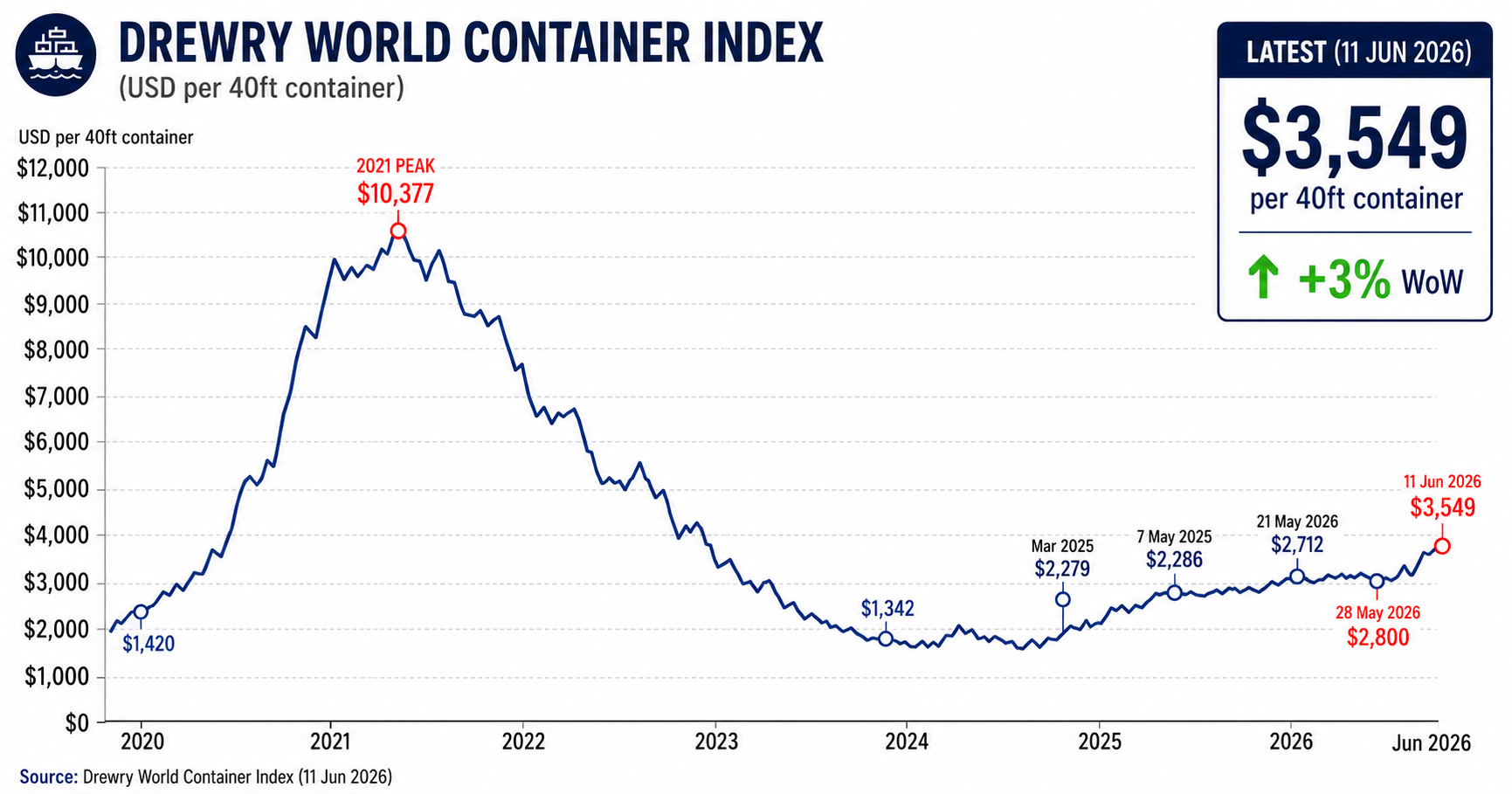

Container shipping rates have largely recovered from the pandemic-era freight crisis but have begun rising again in 2026. While current rates remain far below the 2021 peak, the recent acceleration suggests renewed supply chain pressure that could flow through to automotive costs and vehicle availability.

For the Philippines, where most vehicles and automotive components arrive by sea, higher freight rates can increase landed costs, extend delivery timelines, and reduce inventory flexibility. Early peak-season demand, carrier rate increases, and ongoing geopolitical disruptions are contributing to renewed volatility in global shipping markets.

The recent increase in freight rates reflects a broader rise in logistics costs across global shipping networks. As Hapag-Lloyd noted:

“More broadly, the conflict has increased complexity and costs across the shipping industry, including higher bunker prices, insurance premiums, storage costs, and inland transportation expenses.”

For import-dependent automotive markets such as the Philippines, sustained increases in freight and logistics costs can gradually flow through to vehicle pricing, inventory availability, and delivery lead times. While current conditions are nowhere near the disruption levels seen during the pandemic, the recent upward trend suggests supply-chain pressures may be building again.

Which Brands Are Most Exposed?

Higher exposure: BYD, GAC, MG, Jetour, VinFast, Tesla

Moderate exposure: Kia, Hyundai, Honda, Nissan, Ford

Lower relative exposure: Toyota, Mitsubishi, Isuzu, Suzuki

Brands that rely heavily on imported vehicles are generally more vulnerable to rising freight costs and shipping disruptions, while manufacturers with established ASEAN supply chains may be better insulated from short-term logistics volatility.

Semi Conductor Squeeze is not Over

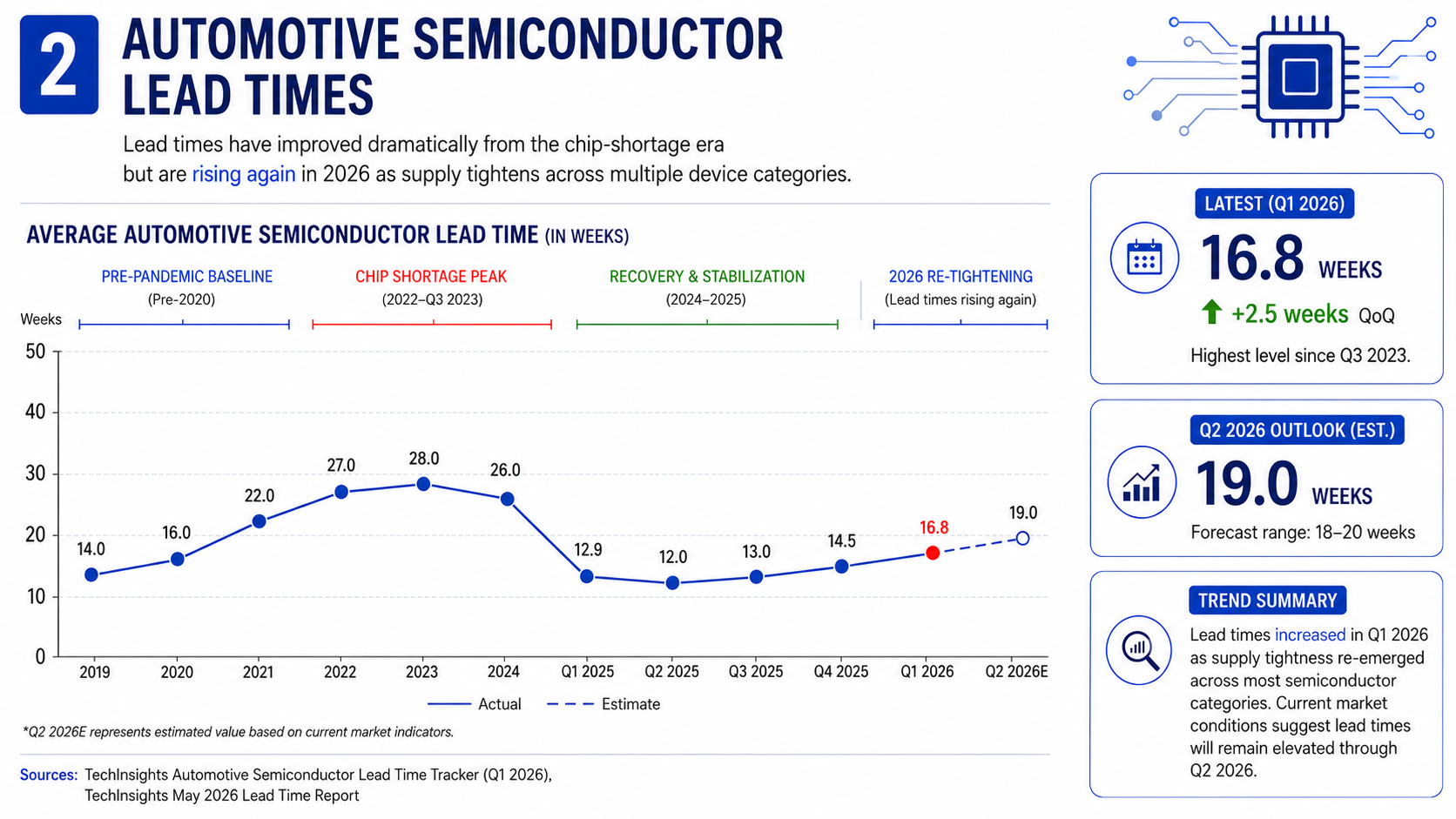

The semiconductor shortage may no longer resemble the crisis conditions of the pandemic, but supply chains have not fully returned to historical norms. Automotive semiconductor lead times rose to 16.8 weeks in Q1 2026, the highest level since Q3 2023, and are expected to remain elevated through Q2 2026. While conditions are far better than the 2022–2023 shortage peak, recent increases suggest supply tightness is beginning to re-emerge across multiple semiconductor categories.

Modern vehicles rely on hundreds of semiconductors across engine management, safety systems, infotainment, sensors, connectivity, hybrid systems, and EV powertrains. As vehicles become increasingly software-defined, even modest disruptions in semiconductor availability can affect production schedules, inventory planning, and vehicle delivery timelines.

A growing concern is the concentration of critical semiconductor materials and supply chains. In April 2026, SK Hynix and Samsung were reported to hold approximately four to six months of helium reserves, helping shield semiconductor production from immediate disruption. While both companies have since diversified supply sources and secured additional inventory, the risk has not disappeared as Qatar remains one of the world's largest helium suppliers, and prolonged disruption to exports through the Strait of Hormuz could still tighten global helium availability and increase costs for semiconductor manufacturers.

AI Is Becoming a Major Competitor for Semiconductor Resources

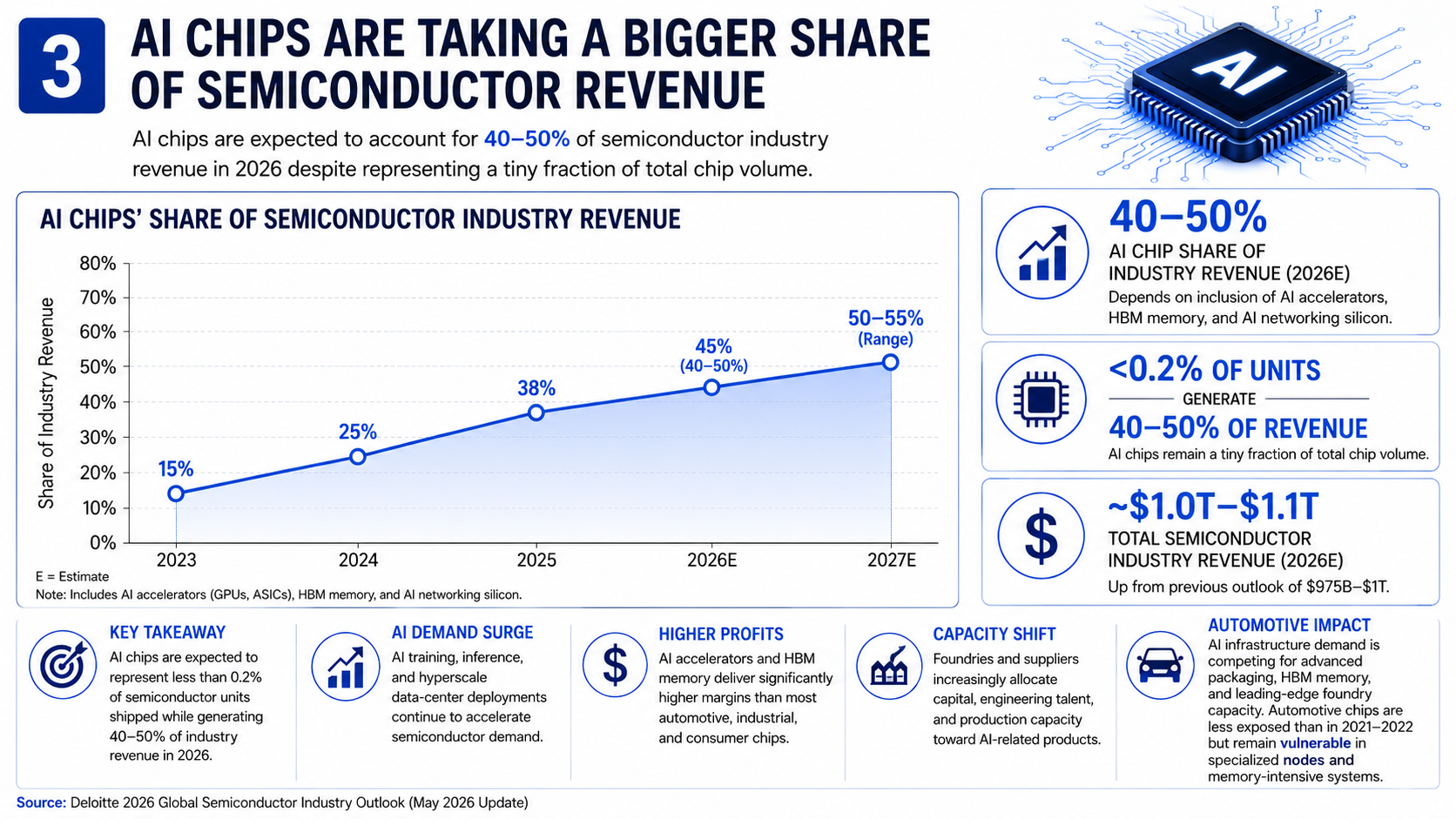

Automakers are no longer competing only with smartphones and consumer electronics for semiconductor resources. The rapid expansion of AI infrastructure is creating a new source of demand for semiconductor investment, engineering talent, advanced packaging capacity, and manufacturing resources.

AI accelerators generate significantly higher revenue and profit per unit than most automotive semiconductors. Deloitte estimates AI chips could account for roughly half of semiconductor industry revenue in 2026 despite representing less than 0.2% of total chip shipments. As a result, foundries and suppliers are increasingly directing capital, R&D spending, and production capacity toward AI-related products.

This does not mean automotive chips are becoming unavailable, however, it does mean the automotive industry may face greater competition for semiconductor investment and capacity, increasing the risk of future supply constraints, longer lead times, and higher component costs.

What Philippine Car Buyers May Notice First

If supply pressures continue through H2 2026, buyers are likely to notice the impact first through pricing, availability, and longer delivery timelines across selected vehicle categories.

- Gradual vehicle price increases

- Fewer discounts and promotional offers

- Longer waiting periods for certain trims and colors

- Tighter allocation for hybrids, EVs, and premium imports

- Reduced availability of high-spec variants dependent on advanced electronics

Not all vehicle categories are equally exposed to these pressures, vehicles with simpler electronics and strong ASEAN production footprints are likely to remain more resilient. Models heavily dependent on imported components, advanced electronics, or limited production allocations may face greater pricing and availability pressure.

Conclusion

The next automotive disruption may not resemble the sudden shutdowns of the pandemic era, but instead the industry appears to be entering a slower-moving, but more persistent supply squeeze driven by energy volatility, shipping instability, structurally tight semiconductor supply, and the rapid expansion of AI demand.

For Philippine buyers, the impact may emerge gradually: higher vehicle prices, fewer promotions, longer waiting times, and tighter availability for hybrids, EVs, and technology-heavy models.

The key risk is no longer a temporary shortage, It is a global automotive supply chain that is becoming structurally more constrained heading into 2027.

Sources

- Anadolu Agency – “Middle East conflict causes massive increases in shipping costs”

- MUFG Research – Philippines oil price and shipping impact analysis

- FedEx Business Insights – Semiconductor challenges in automotive supply chains

- Philippine News Agency – Automotive supply and oil price commentary

- Associated Press – Shipping fuel and logistics disruptions